Credits for trees that were already there

This recently registered ACCU plantation project in WA was planted in 2017. So what makes it eligible to be a carbon project? Especially considering recent regulator attention on additionality. Under a traditional short rotation model, these trees would likely have been harvested for pulp. Under the registered project scenario, harvest is delayed and management moves toward a longer rotation regime.

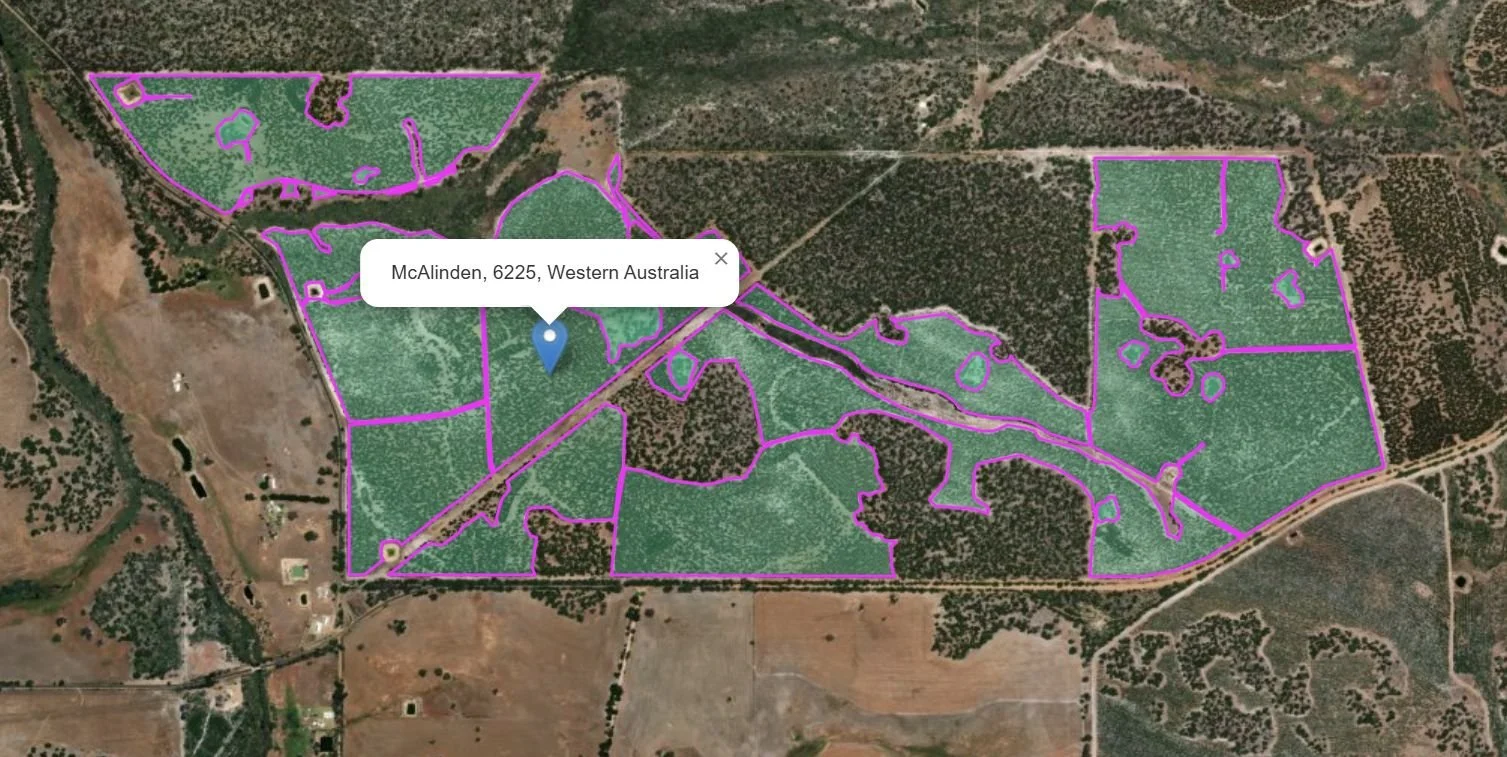

Look at project ERF206323 | Project Explorer | Project Information

It has been registered as a schedule 2 plantation project: i.e. converting an existing short rotation plantation forest to a long rotation plantation forest.

Instead of being harvested in many short rotations it’ll be commercially harvested with at least a further 10 year delay depending on the species. Thinning and pruning will be consistent with long rotation production.

Thinning and pruning can reduce standing carbon in the short term due to removed biomass, but can result in bigger stems that can lift longer term average stocks and harvested wood storage product.

Short term plantations are often harvested for pulp which does not retain carbon for long periods. Relative to the baseline short rotation scenario, carbon stocks over time will be higher and credits will be awarded based on that comparison. There are 63 active plantation projects in Australia under this method and schedule.

The example project referenced in the original post is ERF206323, located around 100 km east of Collie in Western Australia. It involves a blue gum plantation established in 2017 and registered under the ACCU Scheme as a Schedule 2 plantation project.

You can explore the project here:

Project Explorer

https://app.carboneyes.io/project-explorer?project_id=ERF206323&layer=1

Detailed project information

https://app.carboneyes.io/accu/project-information/ERF206323

Under a standard short rotation approach, the crop would usually be harvested early for pulpwood. Under the carbon project pathway, harvest is pushed back and the management intent moves to a longer rotation designed to keep more carbon on site for longer.

Those who followed best practice before the scheme started receive no reward; additionality only

pays for changes from the baseline, not for past good management.

The additionality debate

If the trees were already in the ground, how can credits be justified? The rationale behind the method seems solid. The abatement is not from planting new trees, but from changing management in a way that increases average carbon stocks over time relative to a defined baseline.

The quality of the credits comes down to permanence, additionality, measurement and the presence of co-benefits or co-costs. If the baseline is credible and the management shift is real, the accounting framework supports it.

Why MIS keeps coming up

Many short rotation blue gum plantations now eligible under Schedule 2 trace back to the Managed Investment Scheme (MIS) era of the 1990s and 2000s. Retail capital funded rapid plantation expansion, often supported by favourable tax treatment. When operators such as Great Southern and Timbercorp collapsed during the global financial crisis, confidence in plantation forestry was damaged.

Some plantations were in marginal rainfall zones. Some were poorly managed after collapse. Communities remember that period.

So when an existing blue gum plantation in WA is registered as a carbon project, critics see echoes of MIS. The concern is that carbon income may be layered onto assets that were never commercially robust as fibre systems.

That history does not invalidate the method. But it explains the scepticism.

Market distortion or legitimate signal

Another line of criticism is that plantations in lower growth regions would not be viable without carbon income. That this represents distortion, whether via public purchasing or private capital chasing offsets.

It is worth separating perception from current market structure. Since 2023, Commonwealth purchasing has been a relatively small share of overall ACCU demand, with most buying coming from the private sector. The federal government has also released a significant portion of previously forward contracted units back into the market.

If private entities are paying for delayed harvest and higher carbon stocks, that is a sign from the market. Whether that signal is efficient or optimal for timber supply is a separate question.

There is also a pragmatic industry view: growing out failed short rotation systems to a longer rotation regime may be preferable to clearing them. It may not be transformational forestry reform, but it may still represent a better carbon and land use outcome than reversal.

Fairness of outcomes

Some argue that growers who always intended to manage for long rotation sawlogs receive no carbon benefit for their foresight, while those who pivot from pulp to sawlog can access credits. Those who followed best practice before the scheme started receive no reward; additionality only pays for changes from the baseline, not for past good management.

The same tension appears in soil carbon. Landholders who have spent decades building soil carbon can feel penalised because they cannot demonstrate new abatement relative to a counterfactual.

Without an additionality test any land owner could claim credits and the price of credits would be driven to zero. In that scenario there would effectively be no scheme. But the design challenge remains real: how to preserve incentive while avoiding extreme outcomes.

The ACCU framework allows for new method development, and a new or amended methods could address these gaps.

New or amended methods could address these gaps supported by open and transparent project data.

Transparent project level data matters

Several forestry professionals also raised technical concerns around silviculture timing and timber quality. If pruning and thinning are poorly timed, the assumed uplift in long term storage and higher value product mix may not ever materialise.

Carbon accounting cannot compensate for poor forestry practice. Project level assumptions on growth rates, rainfall, harvest modelling and product allocation need scrutiny.

That is precisely why transparent project level data is important. Projects like ERF206323 are not inherently good or bad. They operate within a defined method with explicit baselines and modelling assumptions.

The debate around them is healthy; it forces sharper thinking about additionality, fairness, timber economics and long term carbon storage.

Carbon markets are policy constructs layered onto biological systems with commercial outcomes. The rules shape behaviour. If stakeholders believe those rules create distortions, the answer is not less transparency, it is imporoved method design, supported by open data.

There are now close to 2,500 active ACCU carbon projects registered in Australia. Roughly 30% of those projects have been issued credits to date. The rest are still in development or early operational phases. Check out our blog article Who is paying for carbon projects in Australia discussing fund–backed ACCU activity and what it means for investors.

References

Carbon Eyes

ACCU project register and project level analytics

Explore project on map | https://app.carboneyes.io/project-explorer?project_id=ERF206323&layer=1

Detailed ACCU project pages with deeper information and official references

More project info| https://app.carboneyes.io/accu/project-information/ERF206323

Want to know more?

30,000 hectares will nearly match Tasmania’s existing plantation projects, read more about it here: Massive new ACCU plantation project announced

Carbon Eyes | ACCU Market Intelligence

Strategic data and integrity signals for the Australian carbon market.

1. Carbon Data Platform

The Foundation of Market Transparency | Access the Platform

A comprehensive view of the ACCU landscape. Access structured CER data, project status and issuance trends. Use our core mapping and analytics to establish your market baseline.

2. Integrity & Market Intelligence

Independent Ratings & Supply Forecasts | Upgrade Your Intelligence

Mitigate risk with our paid intelligence layer. Accessed directly within the Platform, these add-ons provide independent ACCU project ratings and forward looking supply forecasts to guide procurement and investment.

3. Land & Asset Decisioning

Identify the Best Opportunities for Carbon Projects

Carbon Potential Report | View Carbon Potential Report (by address)

Instant, address-based viability assessments for lenders and investors.

Carbon Land Search | Identify & Assess High-Potential Assets

Our premium search engine for institutional funds. Identify and de-risk high-potential carbon assets before acquisition.