What the carbon market revealed this month

Carbon Eyes In the Loop - here’s what you missed

A roundup of our best posts about the carbon market, filtered and in one place. Reach out to the team for more detailed market analysis and further insights.

April saw a busy period across the Australian carbon market, with major ACCU issuances, new project registrations, annual Safeguard compliance data release and continued movement across the method pipeline. This month’s In the Loop pulls together some of the key themes we were tracking across the market, from institutional capital flowing into projects and changing compliance dynamics through to increasing focus on project integrity, permanence and future supply visibility.

Where the streets have no name [28/04/2026]

Record ACCU issuance from projects with suppressed details. ACCUs issued for Environmental Planting (EP) projects spiked in March largely due to 2 Woodside Energy projects with suppressed details: Woodside Pluto Carbon Offset Project - Stage 1 & 2. The projects are in NSW and WA.

The number of credits issued to these 2 projects last month (945 000) is equivalent to the combined issuance of all Australian EP projects for the last 3 years.

EOP100203 I Woodside Pluto Carbon Offset Project - Stage 1

While transparency is a core part of the scheme, the Clean Energy Regulator can suppress specific project information (such as exact spatial boundaries or location data) if an application is made and they are satisfied the suppression is required for one of two reasons:

To protect or respect Aboriginal tradition, or to ensure publication does not threaten, damage or cause harm to a threatened ecological community or threatened species.

Tree cover gain data (see image) may give clues to the location and size of these projects to help establish future EP ACCU supply trends, but there will always be a degree of uncertainty around these estimates.

Suppressed projects remain relatively uncommon across the ACCU scheme, particularly at this scale of issuance. The concentration of such a large volume of EP credits into projects with limited public spatial visibility makes it harder for external market participants to independently assess future supply patterns, estimate project scale, or understand how concentrated future issuance may become within particular regions or proponents.

This becomes more relevant as the ACCU market matures and participants increasingly rely on spatial analysis, land use trends and project level modelling to forecast future supply. Where project boundaries or location details are unavailable, market participants are left relying more heavily on indirect indicators such as vegetation change data, land ownership patterns, issuance timing and regional project clustering (piece together supply trends by looking at concentrations of similar projects in particular areas).

Unlike some engineered methods with more predictable operational profiles, EP projects can accumulate carbon sequestration over long periods before credits are claimed, which means crediting activity can appear in uneven bursts over time, depending on when project proponents choose to submit offsets reports, which means more uneven supply patterns over time. This can contribute to periods where the market appears relatively constrained from an EP issuance perspective, followed by sudden increases in supply when larger projects begin generating credits at scale.

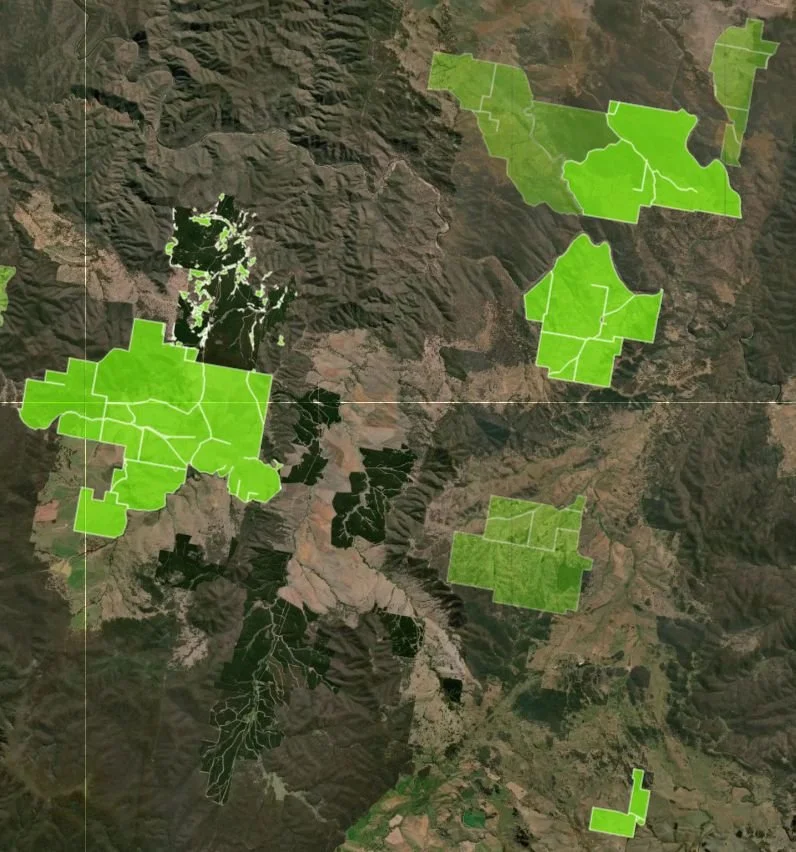

Environmental planting projects: 25 vs 100 years [09/04/2026]

Of the 390 EP projects registered under the ACCU scheme 310 are still active. There is a roughly 60/40 split between 100 year projects and 25 year projects.

In picture: a cluster of EP projects south of Cooma, NSW

Only 56 of all EP projects have been issued credits. But 80% of these are to 100 year projects. The correlation between permanency and issuance in EP projects does not imply causation but it is a trend we will keep an eye on.

Projects selecting a 25 year permanence period receive fewer ACCUs under the scheme due to the permanence discount applied by the Clean Energy Regulator. This affects project economics and may influence financing, land valuation and long term landholder decisions, particularly where projects are being assessed against competing agricultural or development uses over multiple decades. The permanence decision may also interact differently with state based land clearing and vegetation management frameworks, which can vary significantly across jurisdictions and influence both project flexibility and long term land use options for landholders. In some states, existing land clearing restrictions mean that even after the 25 year permanence period ends, vegetation may still effectively remain in place, meaning projects can continue as forested land well beyond the formal crediting obligation period.

The permanence choice can also influence how projects are perceived by different market participants. While both permanence options are recognised under the ACCU scheme, some buyers and investors increasingly place a higher value on longer duration storage profiles, particularly where credits may form part of long term decarbonisation strategies, institutional mandates or public sustainability goals.

Many of the larger institutionally backed projects entering the market are targeting long duration carbon storage profiles, which may be reflected in both the higher number of credits issued to 100 year projects and the premium these credits often attract in the market due to demand for high integrity credits representing quality and permanence.

Over time, this contributes to greater differentiation between ACCUs at a method and project level, particularly as larger buyers become more selective around permanence, project transparency, reversal risk and broader perceptions of credit integrity.

A busy period for the Australian carbon market [13/04/2026]

On the 14th April, the Clean Energy Regulator will publish the full 2024-25 Safeguard Mechanism data. That matters not just for Safeguard participants (emitters), but for anyone trying to understand near term ACCU and SMC demand, compliance behaviour and market positioning.

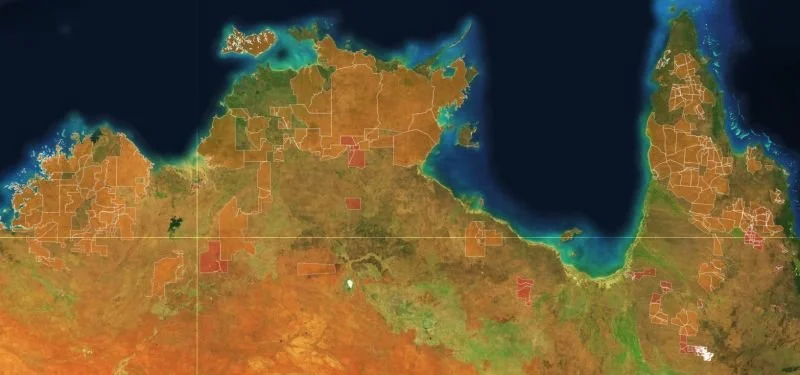

Last week saw the release of two new savanna fire management methods. These are important updates: they bring in newer science, recognise more carbon pools, and could materially change the future ACCU supply of existing projects (see image) which currently account for 7% of ACCUs issued.

As well as the new savanna fire management methods, the government has renewed focus on livestock methane methodologies, with work underway to rebuild the beef herd method. The broader method pipeline is also moving, with work continuing on IFLM, Improved Native Forest Management, and other proponent led method reforms.

Method reform is increasingly becoming one of the key market drivers because changes to baselines, measurement rules, permanence settings and eligible carbon pools can materially alter forecasted project economics and future ACCU supply expectations. Even relatively technical methodological adjustments can have significant downstream impacts on issuance profiles, project viability and the attractiveness of certain methods to investors and developers.

This is particularly important for secondary ACCU buyers and investors trying to model reliable long term supply and the variances across different methods. As the market matures, participants are increasingly looking beyond total ACCU volumes and focusing more closely on where future supply is likely to come from, how durable that supply may be, and how different methods may perform under evolving policy, integrity and market expectations.

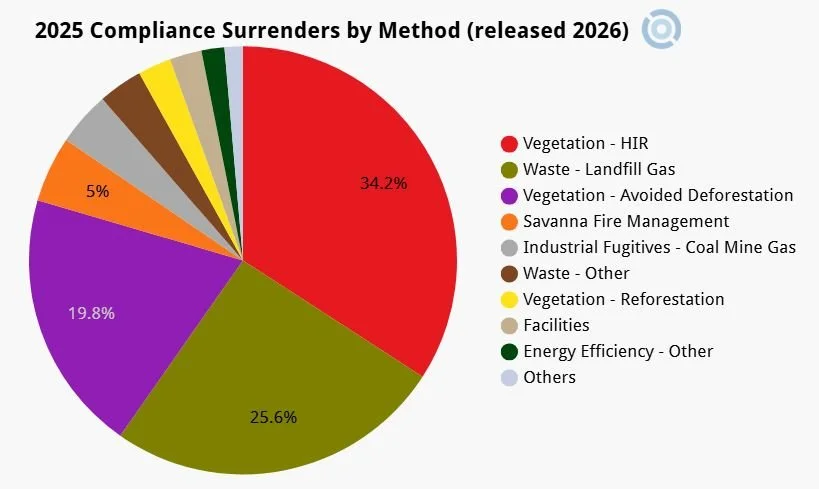

Which ACCUs are being surrendered for Safeguard compliance [20/04/2026]

Of the 10.78m ACCUs surrendered to meet compliance obligations in the latest Clean Energy Regulator data release roughly 1/3 were credits from Human-Induced Regeneration (HIR) projects.

The share of the total surrenders for the dominant 3 methods broadly reflected the share that those 3 methods had in ACCU project issuance during the same period and leading into the recent compliance deadline.

The tapering of ACCU issuance for the Avoided Deforestation method is reflected in the drop in overall representation to 19.8% from 27.6% in the previous reporting period for cancellations. In absolute terms there was a slight increase.

The alignment between issuance composition and surrender composition suggests the market is still heavily influenced by current supply availability rather than strong method level differentiation during compliance purchasing. For example, HIR projects continue to make up a large share of both ACCU issuance and Safeguard surrenders, reflecting the volume of credits historically available from the method rather than a specific preference for HIR credits themselves.

As issuance from legacy methods like HIR slows over time, the composition of surrendered ACCUs may gradually move towards newer project types entering the market, particularly if those methods begin contributing a larger share of overall supply.

Surrenders method-composition is also likely to reflect expectations around future market perception changes e.g. if the market believes that EP ACCUs are likely to become more sought-after in future there would be a incentive to hold EP ACCU's and surrender ACCUs sourced from other methods

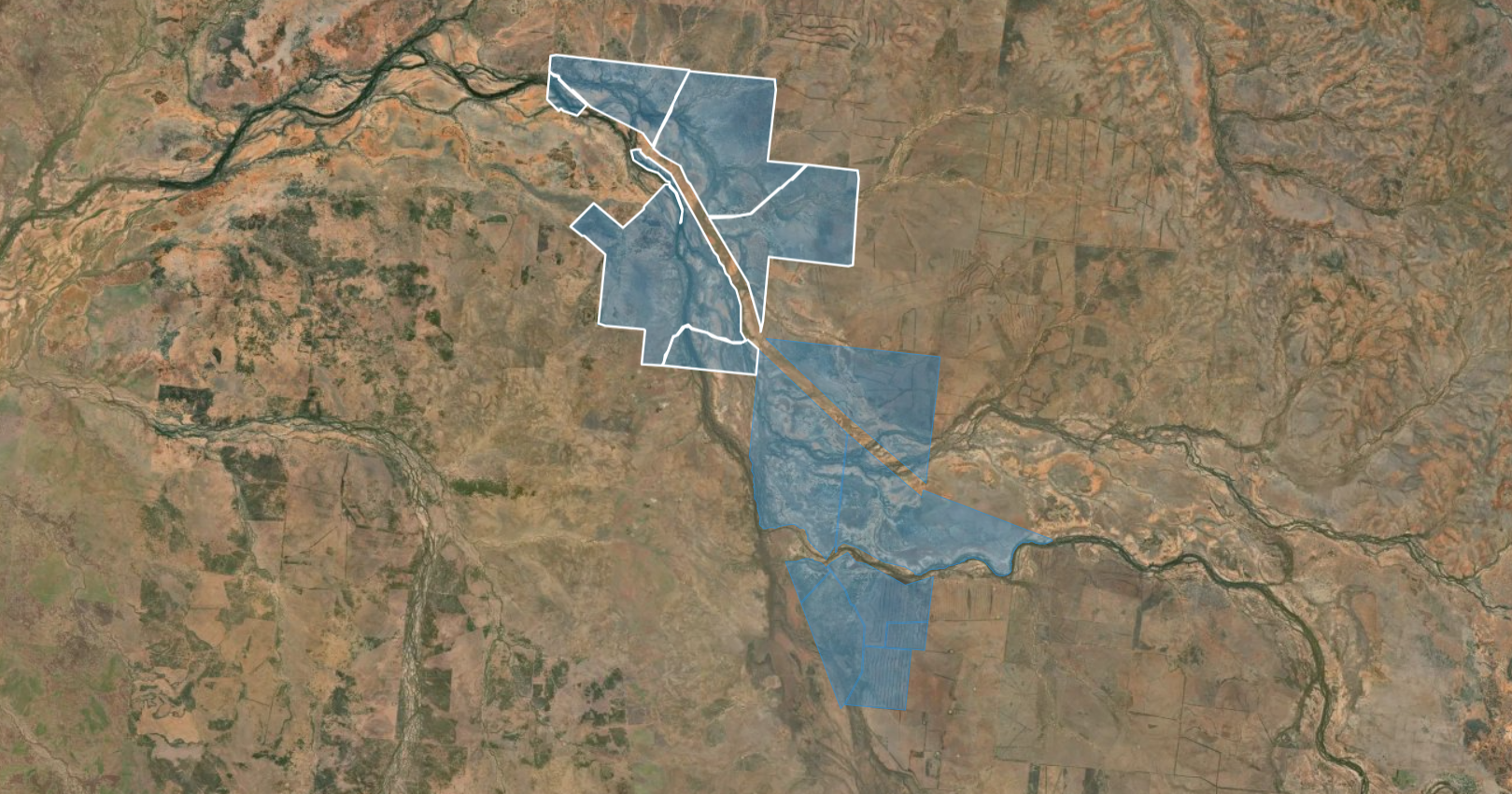

Image from the Austin Down Station Regeneration Project:

ERF121665 | Project Information I Project Explorer

Austin Downs Station Regeneration Project is a Human-Induced Regeneration project located on a pastoral lease approximately 17km northwest of Cue in the Murchison region of Western Australia. It was registered in May 2018 and covers a project area of 157,561.89 hectares.

Human-Induced Regeneration (HIR) projects establish permanent native forests through assisted regeneration. This method requires the land to not have had forest cover at any time for at least 10 years prior to the project commencing. The project achieves regeneration from in-situ seed sources, including rootstock and lignotubers, primarily through managing the timing and extent of livestock grazing to allow the native forest to recover. Read more…

27 New ACCU projects in latest register update [22/04/2026]

Two adjacent soil projects by CarbonLink™ cover a massive 37 000 ha, representing almost 4% of all land under active soil ACCU projects.

The image shows Moonbira and Avondale, two of the three new soil projects registered by CarbonLink™ in March 2026

Moonbria Soil Carbon Project is a soil carbon project located approximately 65km south-west of Barcaldine in central-western Queensland, and covers an expansive 18,508.27 hectares. Read more…

Avondale Soil Carbon Project is a soil carbon project located approximately 40km northwest of Blackall and 90km south-southwest of Barcaldine in the Central West region of Queensland, and covers a vast area of 18,565.28 hectares. Read more…

Wildhorse Soil Carbon Project is the third soil carbon project located on the "Wildhorse" property, approximately 30km southwest of Rolleston in the Central Highlands region of Queensland, and covers a project area of 4,543.50 hectares. Read more…

There is also a spike in new waste diversion projects (process source separated organic waste so it avoids landfill methane) - with 8 projects added.

There are 3 new Environmental Planting projects with 2 of these being large scale: 3552 ha (SA) by Carbon Neutral and 2819 ha (WA) backed by Japanese oil and gas company INPEX Corporation. Small scale plantation projects mostly by Landari make up the rest of the new projects.

The scale of some of the newer soil projects (CarbonLink™) goes against a trend seen over the last year which saw a move towards smaller adjacent projects rather than single large projects. AgriProve led this trend. Larger aggregated projects can spread fixed costs such as soil sampling, modelling, auditing and project management across a much bigger land base, which can improve project viability compared to smaller standalone projects. Larger projects however allow for less variability in management techniques across different terrain. This is particularly relevant in soil carbon where measurement costs and variability between properties can materially impact project economics.

The rise in waste diversion registrations also continues the broader trend towards engineered and infrastructure linked methods alongside traditional land based carbon sequestration projects. Unlike many land sector projects, these methods are often connected to physical processing infrastructure, continuous operational systems and more direct measurement approaches. This can change both the capital profile and risk profile of projects entering the ACCU market, particularly as larger industrial operators and institutional investors become more involved.

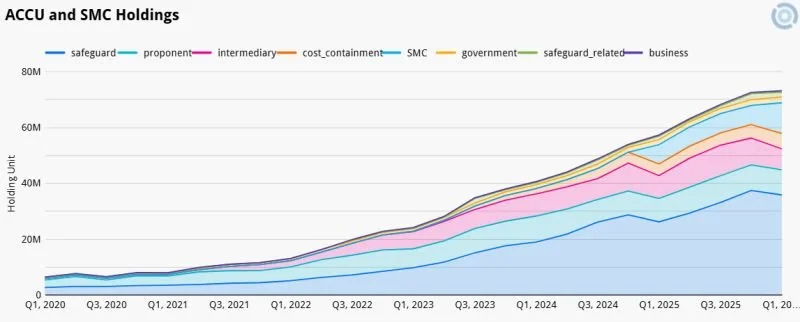

Australian carbon credit holdings remain stable [23/04/2026]

Despite the recent robust levels of ACCU cancellations (offsetting by emitters to meet Safeguard obligations) the overall holdings of credits (ACCUs + SMCs) have marginally increased in Q1 2026.

The increase in the quarter is almost all due to SMC issuance: 6.7m were issued while only 2.57m were cancelled. SMCs are prescribed carbon units awarded under the scheme's safeguard rules to emitters who beat their emissions reduction benchmarks.

From a compliance point of view SMCs are fungible with ACCUs. The data suggests most emitters beating their Safeguard benchmarks are choosing to keep their SMCs for future use rather than trade them.

The growing stockpile of SMC holdings is becoming increasingly relevant to forward ACCU demand modelling because retained SMCs are effectively acting as future compliance inventory. Rather than immediately selling or cancelling these credits, many facilities appear to be holding them for future Safeguard compliance obligations, particularly as baselines change over time. This creates an additional layer of potential supply within the compliance market that sits outside the ACCU project pipeline itself.

This also means that the headline compliance demand figures don’t always translate directly into immediate ACCU purchasing pressure in the spot market. A facility with a growing bank of SMCs may be able to meet part of its future compliance obligations internally without needing to purchase ACCUs at the same scale. As SMC balances grow across the system, understanding how participants choose to hold, trade or surrender these units may become increasingly important for interpreting future ACCU demand dynamics.

Over the longer term however, many facilities are still expected to require increasing volumes of offsets as Safeguard baselines tighten and lower cost internal abatement opportunities are exhausted. In this sense, SMC holdings may act more as a timing buffer rather than a permanent substitute for ACCU demand.

There is also growing evidence that some emitters are becoming more selective around the types of ACCUs they are willing to purchase, particularly where credits may ultimately be used for voluntary claims, public sustainability commitments or investor scrutiny in addition to compliance. This is increasing focus on project integrity, permanence, transparency and reversal risk across different methods.

For larger buyers, long term procurement strategies are also increasingly tied to price hedging and future supply security. Securing access to projects or preferred ACCU types earlier may help reduce exposure to future price volatility, particularly if supply from some legacy methods continues to decline over time.

The reversal risk associated with some carbon sequestration projects is also becoming more important as part of procurement decisions. While the ACCU scheme contains permanence obligations and buffer mechanisms, buyers may still consider the reputational implications of relying heavily on projects that later face carbon loss events, project underperformance or broader integrity scrutiny.

The ACCU market continues to evolve quickly, with changes in project scale, method reform, institutional participation and compliance behaviour all shaping how future supply and demand may develop. What stands out is that the market is becoming increasingly differentiated at a project and method level, with more attention being placed on integrity, permanence, transparency and long term supply reliability. As always, we will continue tracking the underlying project data, register movements and policy developments shaping the Australian carbon market.

For more comprehensive market insights and analysis, please get in touch at info@carboneyes.io.

Check out our blog article Who is paying for carbon projects in Australia discussing fund–backed ACCU activity and what it means for investors.

References

Carbon Eyes ACCU project register and project level analytics

Carbon Eyes market commentary on ACCU project activity and issuance trends

CER (Clean Energy Regulator)

DCCEEW (Department of Climate Change, Energy, Environment and Water)

Federal Register of Legislation: Carbon Credits (Carbon Farming Initiative) Rule 2015

Section 93A(2) of CFI Rule 2015: the information the CER must publish on the ACCU Scheme project and contract registers.

Federal Register of Legislation: Carbon Credits (Carbon Farming Initiative) Act 2011

Section 76(1) & 76(2) of CFI Act 2011: reporting periods can be chosen by the proponent, provided they are not shorter than 6 months and not longer than 5 years.

Section 16(2) of CFI Act 2011: formula for calculating unit entitlement & 20% discount for a 25-year projects.

Sections 86A and 87 of CFI Act 2011: defined permanence periods.

Sections 90 and 91 of CFI Act 2011: requirement to relinquish units if a reversal of sequestration occurs due to natural disturbances / conduct.

Federal Register of Legislation: National Greenhouse and Energy Reporting Act 2007

Safeguard Mechanism Credits (SMCs): Act incentivising Australia’s largest emitters to reduce emissions below their set baselines.

Want to know more?

Check out New environmental planting project to boost ACCU supply discussing what large-scale plantings tell us about supply.

Carbon Eyes | ACCU Market Intelligence

Strategic data and integrity signals for the Australian carbon market.

1. Carbon Data Platform

The Foundation of Market Transparency | Access the Platform

A comprehensive view of the ACCU landscape. Access structured CER data, project status and issuance trends. Use our core mapping and analytics to establish your market baseline.

2. Integrity & Market Intelligence

Independent Ratings & Supply Forecasts | Upgrade Your Intelligence

Mitigate risk with our paid intelligence layer. Accessed directly within the Platform, these add-ons provide independent ACCU project ratings and forward looking supply forecasts to guide procurement and investment.

3. Land & Asset Decisioning

Identify the Best Opportunities for Carbon Projects

Carbon Potential Report | View Carbon Potential Report (by address)

Instant, address-based viability assessments for lenders and investors.

Carbon Land Search | Identify & Assess High-Potential Assets

Our premium search engine for institutional funds. Identify and de-risk high-potential carbon assets before acquisition.